Interest Rate Variability

Interest rates can fluctuate due to economic policies and market conditions.

Although current rates may seem high, there is no guarantee that they will drop significantly in the short term. Central bank decisions, inflation, and other global economic factors can influence interest rates.

For example, if the central bank decides to raise rates to fight inflation, mortgage rates could climb even higher, making monthly payments even more expensive.

The possibility of rates decreasing in the future is one of the reasons why buying a home now can be beneficial. If you buy now, you can take advantage of today’s home prices and, when rates drop, you can refinance your mortgage to lower your monthly payments. This allows you to benefit from property appreciation while keeping long-term financing costs under control.

Interest Rate Variability

Interest rates can fluctuate due to economic policies and market conditions.

Although current rates may seem high, there is no guarantee that they will drop significantly in the short term. Central bank decisions, inflation, and other global economic factors can influence interest rates.

For example, if the central bank decides to raise rates to fight inflation, mortgage rates could climb even higher, making monthly payments even more expensive.

The possibility of rates decreasing in the future is one of the reasons why buying a home now can be beneficial. If you buy now, you can take advantage of today’s home prices and, when rates drop, you can refinance your mortgage to lower your monthly payments. This allows you to benefit from property appreciation while keeping long-term financing costs under control.

Advantages of Buying Now

Buying a home now, despite current interest rates, can offer several advantages that are often overlooked. Let’s look at some of the reasons why this can be a smart strategy:

Access to Available Properties

Less Competition

In a higher interest rate environment, buyer competition can be lower. This means you may have more options and face fewer bidding wars. Imagine you’re interested in a home in a highly sought-after neighborhood.

In a low-rate market, it’s likely there would be multiple competitive offers for that same house, driving the final price higher. In contrast, with higher rates, there are fewer buyers competing, which can give you an advantage.

You may be able to negotiate the purchase price and sales terms with more ease, increasing your chances of getting the home you want without entering a bidding war.

Opportunities in Inventory

With fewer active buyers in the market, you might find more properties available. This gives you more negotiation power in terms of price and conditions.

For example, you may come across sellers who are more willing to offer incentives, such as helping with closing costs or making repairs, to attract the limited pool of buyers. In addition, in a less competitive market, you can take the necessary time to evaluate several options and choose the one that best fits your needs and budget.

Building Equity

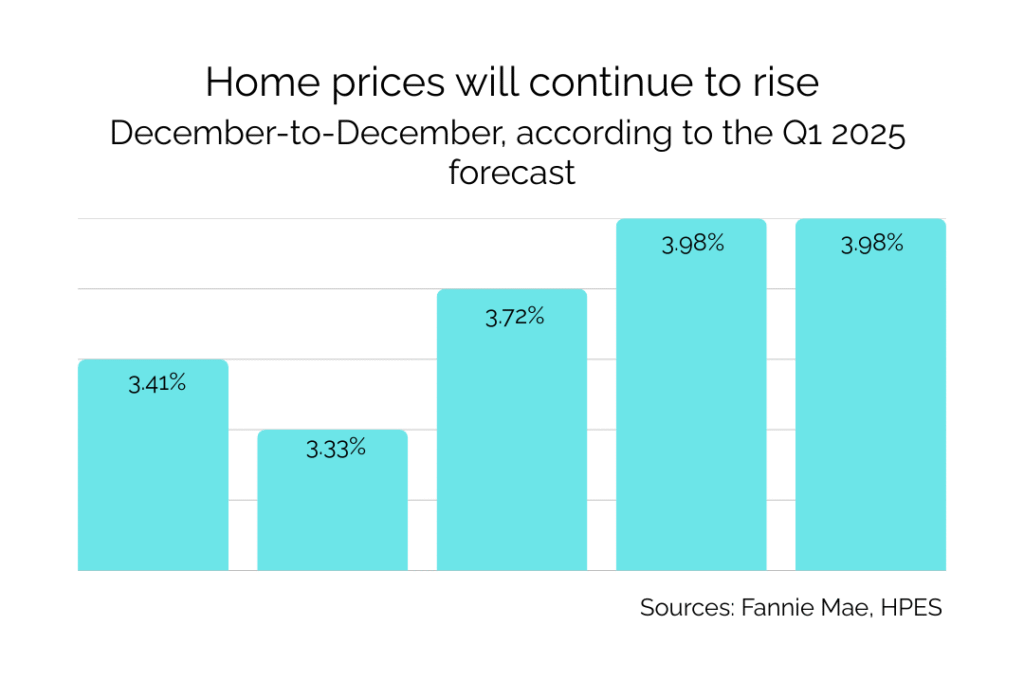

Increase in Property Value

By buying now, you start building equity right away. As you pay down your mortgage and your property value increases, your net worth also grows. Suppose you buy a home for $600,000. If the market’s annual appreciation rate is 3%, in five years your home’s value could rise by nearly $100,000. During that time, you will also have reduced the principal on your mortgage, further increasing your equity.

![eBook How to Increase Home Value [7 Simple Ways]](https://realestatejuanc.com/wp-content/uploads/2022/03/FORMAS-WAYS-TO-INCREASE-YOUR-HOME-VALUE.png)